Chicago Public Schools (CPS) does not receive revenues when it pays expenses. As a result, CPS’ cash flow goes through peaks and valleys throughout the year, depending on when revenues and expenditures are received and paid. Further, revenues are generally received later in the fiscal year while expenditures, mostly payroll, are level across the fiscal year––with the exception of debt service and pensions. The timing of these two large payments (debt service and pensions) occurs just before major revenue receipts. These trends in revenues and expenditures put cash flow pressure on the district.

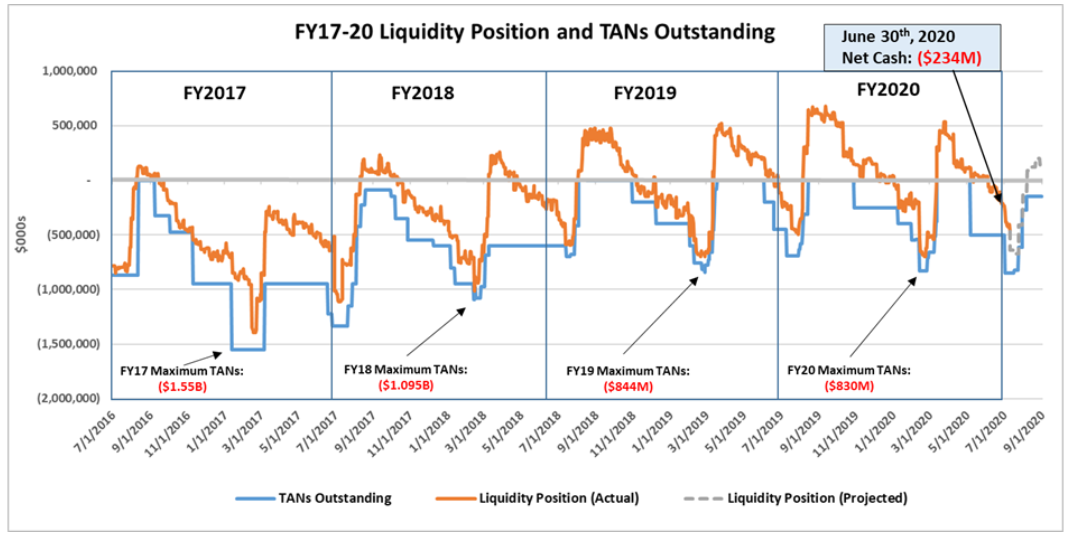

Over the past three years, CPS has reduced its short-term borrowing by approximately $700 million. Despite the unprecedented circumstances related to COVID-19 in the last quarter of FY2020, the district continued to make progress on improving its cash flow by relying less on short-term borrowing and saving approximately $2 million in short-term interest costs. While CPS continued to use short-term borrowing to support liquidity and operations, the district reduced its short-term borrowing in FY2020 by $14 million, declining to $830 million from $844 million in FY2019. CPS spent approximately four months of the year without short-term borrowing.

In FY2020, approximately $3.8 billion, or 67 percent of CPS’ current year revenues, excluding non-cash items, were received after February, more than halfway into the fiscal year. The annual debt service payment is made in mid-February, just prior to the receipt of approximately $1.4 billion of the first installment of property tax revenues. The annual Chicago Teachers’ Pension Fund (CTPF) pension payment is made in late June, just before CPS receives approximately $1.3 billion of the second installment of property taxes (which are due August 3, 2020).

Historically, approximately 49 percent of the Chicago Board of Education’s budgeted expenditures are for payroll and associated taxes, withholding, and employee contributions. In addition, the Board’s recurring expenses for educational materials, charter school payments, health care, transportation, facilities, and commodities total approximately 41 percent of the Board’s budgeted expenditures. The timing of these payments is relatively predictable and spread throughout the fiscal year. Approximately 10 percent of budgeted revenues, which flow through the operating account, are comprised of debt service, annual pension payments, and interest on short-term debt.

Most organizations set aside reserves in order to weather the peaks and valleys in cash flow. Board policy requires that the Board maintain an operating reserve of at least five percent of the total operating and debt service budget, and the Government Finance Officers Association (GFOA) recommends reserve levels between five and 15 percent of spending. The Board is in the process of updating its fund balance policy to better align itself with the GFOA recommendations. As of June 30, 2020, the district projected that the general fund balance totaled $524 million and that CPS has approximately $266 million of cash, with $500 million in short-term borrowing outstanding.

Revenues

CPS has three main sources of operating revenues: local revenues, state revenues, and federal revenues.

- Local Revenues: Local revenues are largely made up of property taxes. CPS receives $3.27 billion of property taxes every year, of which $2.7 billion is issued to the Board’s operating fund, $490 million is distributed to the CTPF through the pension levy, and $61 million is allocated to capital projects through the Capital Improvement Tax levy. The Board receives property tax revenues in two installments, 96 percent of which are received from February onwards, over halfway through the fiscal year. The first installment of approximately $1.4 billion is due March 1 and is received into the main operating account in late February or March. The second installment of approximately $1.3 billion is typically received in July or August, depending on the deadline. Property tax receipts have grown from $2,352 million in FY2012 to a projected $3,265 million in FY2021, a compounded growth rate of 3.7 percent.

- State Revenues: State revenues are largely comprised of Evidence-Based Funding (EBF) and state grants. EBF is received regularly from August through June in bi-monthly installments. In FY2020, EBF totaled approximately 84 percent of the state revenues received by CPS, up from 57 percent in FY2017 before EBF was created. This increase improves cash flow due to the consistency of the payments. Block grant payments are distributed sporadically, and approximately $50 million of block grants were vouchered but not disbursed to CPS as of June 30, 2020.

- Federal Revenues: The state administers categorical grants on behalf of the federal government once grants are approved. In three of the last four fiscal years, federal revenues were not received until about halfway into the fiscal year. In FY2020, only approximately $39 million of the $733 million of federal revenues were received before January 2020. In spring of 2020, CPS was awarded $206 million of CARES Act federal funds related to COVID-19. As of June 30, 2020, no CARES Act funds have been received, and the Board anticipates receipt of these monies during FY2021.

- Working Capital Short-Term Borrowing: The district has the ability to issue short-term borrowing in order to address liquidity issues. Short-term borrowing allows the Board to borrow money to pay for expenditures when cash is not available and then repay the borrowing when revenues become available. State statute provides CPS with the ability to issue this type of cash flow borrowing through a Tax Anticipation Note (TAN). In FY2020, CPS issued a maximum of $830 million in TANs to support liquidity, a decrease of $14 million from FY2019 which saved $2 million in interest expenses. TANs are repaid from the district’s operating property tax levy. In response to COVID-19, Cook County waived all late penalties and fees against late property tax payments until October 1, causing uncertainty around the timing of the second installment of property taxes. To support liquidity in FY2021, CPS is prepared to issue TANs against the second installment property taxes as the need arises. This will allow the Board to maintain liquidity despite the uncertainty of the timing of the property tax revenues from July through October. Short-term borrowing requires that CPS pays interest on these bonds. In FY2021, the Board budgeted approximately $19 million in interest costs for the TANs.

Expenditures

CPS expenditures are largely predictable, and the timing of these expenditures can be broken down into three categories: payroll and vendor, debt service, and pensions.

- Payroll and Vendor: Approximately $3.8 billion of CPS’ expenditures are payroll and associated taxes, withholding, and employee contributions. These payments occur every other week, and most of the expenditures are paid from September through July. Approximately $1.8 billion of CPS vendor expenses are also relatively stable across the year.

- Debt: Debt service is deposited into debt service funds managed by independent bond trustees. These debt service deposits are backed by Evidence-Based Funding and are deposited once a year. In FY2020, the debt service deposit from EBF was approximately $392 million in mid-February. The timing of this debt service deposit comes just before CPS received approximately $1.4 billion in property tax revenues. The remainder of the bonds are paid by personal property replacement taxes and/or property taxes that are deposited directly with the trustee, meaning they do not pass through the district’s operating fund from a cash perspective. The timing and amount of these payments are dictated by the bond documents. Once the trustees have verified that the debt service deposit is sufficient, they provide a certificate to the Board which allows the Board to abate the backup property tax levy that supports the bonds.

- Pensions: In FY2020, approximately $80 million of the pension payment was made on June 26, 2020, while approximately $13.9 million of the pension payment was made previously during FY2020. The timing of the bulk of the pension payment comes just before CPS receives approximately $1.3 billion in property tax revenues. In FY2020, a dedicated pension levy will directly intercept $490 million in revenue to the CTPF—these revenues do not pass through the district’s operating funds from a cash perspective. The dedicated pension levy plus the state funding for pensions means that 84 percent of CPS’ pension obligation is currently funded by structural funding sources. The Board will contribute $60 million in August 2020 to the Municipal Employees’ Annuity and Benefit Fund (MEABF) due to the City no longer picking up the full employer pension costs for CPS.

Forecasted Liquidity

The chart below provides CPS’ liquidity profile from FY2017 to FY2020. As shown in the chart below, the district spent approximately five months in a net positive cash flow position in FY2020. As noted earlier, the total short-term borrowing was lowered by $14 million in FY2020—from $844 million of maximum borrowing in FY2019 to $830 million in FY2020.

Chart 1: FY2017–FY2020 Operating Liquidity Position