CPS’ Capital Improvement Program, described in the Capital chapter, funds long-term investments that provide our students with a world class education in high-quality learning environments. CPS relies on the issuance of bonds to fund the investments laid out in our Capital Improvement Program, which include roofs, envelopes, and windows; state-of-the-art high school science labs; high-speed internet and digital devices; playgrounds and athletic fields; and expansion of full-day Pre-K and other high-quality programmatic investments. Bonds are debt instruments that are similar to a loan, requiring annual principal and interest payments.

Debt Overview

As of June 30, 2020, the Board of Education has approximately $8.1 billion of outstanding long-term debt and $500 million of outstanding short-term debt. FY2020 includes appropriations of $711 million for debt service payments on alternate bonds and capital improvement tax bonds.

In FY2018, due to advocacy from parents, educators and courageous elected officials from Chicago and throughout the state, the State of Illinois approved Public Act 100-465 (PA 100-465). This created a new funding formula for school districts throughout the state, including CPS. The new Evidence-Based Funding formula (EBF or EBF Formula) replaces the prior General State Aid (GSA) formula. As a result of PA 100-465 and the EBF Formula, most of the outstanding CPS bonds that were previously repaid from GSA revenues will now be paid by EBF revenues going forward.

The EBF formula provides more funding stability for the Board’s fixed costs, including capital, but it is also a major revenue source for core academic priorities. Therefore, CPS can more effectively balance day-to-day classroom needs with the need for quality education facilities.

To continue to improve school facilities and lessen the impact of future debt service repaid from the district’s operating budget, CPS will use the statutorily-authorized annual Capital Improvement Tax (CIT) levy that the Board approved in FY2016 to aid in funding its ongoing Capital Improvement Program. In FY2017, the Board issued its first series of Capital Improvement Tax bonds (CIT bonds). As of June 30, 2020, a total of three series of CIT bonds have been issued. The CIT bonds are further described below.

Types of Obligations

The Board is authorized by state law to issue notes and bonds and to enter into lease agreements for capital improvement projects.

As with most school districts, CPS issues bonds backed by the full faith and credit of the Board, otherwise known as General Obligation (GO) bonds. These GO bonds are paid for from all legally available revenues of the Board.

CPS also issues a special type of GO bond called an “alternate revenue” GO bond. These bonds are backed by two revenue sources and offer a number of other bondholder protections.

The first revenue source that is supporting CPS bonds is one of the following: EBF, Personal Property Replacement Taxes (PPRT), revenues derived from intergovernmental agreements with the City of Chicago, property taxes, and federal interest subsidies. The majority of CPS bonds are backed by EBF. In FY2021, approximately $446 million in EBF revenues will be required for debt service, compared to $382 million in FY2020 and $283 million in FY2019. In addition to debt service funded by EBF, $39 million of debt service will be paid from PPRT in FY2021. Debt service paid from PPRT revenues also reduces PPRT revenues available for operating purposes. Additionally, $142 million in debt service will be paid by revenue resulting from Intergovernmental Agreements with the City of Chicago.

The second revenue source for all CPS alternate revenue GO bonds is a property tax levy which is available to support debt service should the first pledge of revenue not be available. On an annual basis, when the first source of revenue is available to pay debt service, the property tax levy will be abated and not extended, as it has been every year.

The Board is authorized to issue alternate revenue bonds after adopting a resolution and satisfying public notice publication and petition period requirements in lieu of a voter referendum, which is typical in other school districts. The bonds are also supported by the GO pledge of the Board to use all legally available revenues to pay debt service.

The Public Building Commission (PBC) of the City of Chicago, is a local government entity which manages construction of certain school and other public building projects. In the past, the PBC has sold bonds which rely on CPS property tax levies. No PBC bonds have been issued since 1999, and no additional issues are under consideration. In FY2020, CPS made its last PBC bond payment from property tax revenues received in FY2019. Accordingly, the FY2021 budget, and those going forward, will contain no appropriations for principal and interest on PBC bonds.

CPS has benefited from issuing bonds with federal interest subsidies, resulting in a very low cost of borrowing. These include Qualified Zone Academy Bonds (QZABs), which provide capital funding for schools in high poverty areas; Qualified School Construction Bonds (QSCBs); and Build America Bonds (BABs)––the latter two created by the American Recovery and Reinvestment Act of 2009 (ARRA). With the expiration of ARRA, new QSCBs and BABs are no longer available, although the federal government continues to pay the interest subsidy to CPS. The FY2021 budget includes $25 million of federal subsidies for debt service.

In FY2016, CPS began levying a Capital Improvement Tax (CIT) levy to fund capital projects. After the CIT was authorized by the City Council, it generated $45 million in its initial year. In FY2017, CPS sold the first series of dedicated revenue CIT bonds to fund capital projects, with additional issues sold in subsequent years. As of June 30, 2020, CPS has sold three series of CIT bonds, and the total amount of CIT bonds outstanding is $880 million.

The FY2021 budget includes a CIT levy and appropriations of approximately $51 million to pay debt service on CIT bonds. The CIT bonds are not alternate revenue GO bonds. They are limited obligations of the Board payable solely from the CIT levy. As a result of the structure, the CIT bonds carry a bond rating of “A-,” allowing CPS to achieve a lower borrowing cost.

Debt Management Tools and Portfolio

As part of the Debt Management Policy, CPS is authorized to use a number of tools to manage its debt portfolio including refunding existing debt, issuing fixed or variable-rate bonds, and issuing short-term or long-term debt. These tools are used to manage various types of risks, generate cost savings, address interim cash flow needs, and assist capital asset planning.

Typically, CPS issues long-term fixed-rate bonds, which pay a set interest rate according to a schedule established at the time of debt issuance. However, CPS has also periodically issued long-term bonds with a variable rate structure whereby the interest rates in a short-term mode are established pursuant to a margin over an index for a predetermined amount of time. In September 2019, CPS refunded its last outstanding variable-rate series with fixed rate bonds. As of June 30, 2020, all CPS outstanding debt is fixed rate.

Credit Ratings

Credit rating agencies are independent entities, and their purpose is to give investors or bondholders an indication of the creditworthiness of a government entity. A high credit score can lower the cost of debt issuance, much the same way a strong personal credit score can reduce the interest costs of loans and credit cards. Ratings consist of a letter “grade,” such as A, BBB, BB, or B, and a credit “outlook,” or expectation of the direction of the letter grade. Thus, a “negative outlook” anticipates a downgrade to a lower letter grade, a “stable outlook” means the rating is expected to remain the same, and a “positive outlook” may signal an upgrade to a higher, better rating.

In FY2018, State of Illinois education funding reform was approved by the State Legislature. Because education funding reform provided an entirely new EBF Formula, an increase in the required State contribution to CPS teachers’ pensions, and the ability for CPS to collect a pension property tax levy, CPS is on much stronger financial footing.

CPS meets frequently with the credit rating agencies about its budget, audited financial results, debt plan, and management initiatives to ensure the agencies have the most updated information possible. The rating agencies take several factors into account in determining any rating, including management, debt profile, financial results, liquidity, and economic and demographic factors. In FY2020, CPS received general obligation credit rating upgrades from Fitch Ratings (BB Stable), Moody’s (B1 Stable), and Standard and Poor’s (BB- Stable). Kroll Bond Rating Agency currently rates CPS general obligation bond series issued since 2016 BBB Stable, and all older CPS general obligation bonds BBB- Stable.

In addition to the CPS general obligation bond rating, the CIT bonds––which were first issued in FY2017 as a new and separate credit structure from the existing CPS general obligation credit––contain a separate and distinct credit rating. The CIT credit structure received an investment grade rating from two rating agencies at inception in FY2017. Currently, Fitch Ratings rates the CIT credit A- Stable and Kroll Bond Rating Agency rates the CIT credit BBB Stable.

FY2021 Liquidity and Short-term Borrowing

CPS issues Tax Anticipation Notes (TANs) to cover operating cash flow needs. The notes are repaid from property taxes. CPS reduced its maximum outstanding short-term borrowing to $830 million in FY2020 from $844 million in FY2019. CPS will continue to issue TANs in FY2021 to cover operating cash flow needs.

FY2021 Debt Service Costs

As shown in the table below, FY2021 includes total appropriations of approximately $711 million for alternate bonds, CIT bonds, and PBC payments.

CPS is required to set aside debt service one year in advance for EBF-funded debt and 1.5 years in advance for PPRT and CIT bond-funded debt service. The FY2021 revenues shown for the debt service funds will be set aside for these future debt payments, which are required by bond indentures to be held in trust with an independent trustee. PPRT, used to pay alternate revenue bonds, is deposited directly from the State to a trustee; and the CIT levy, used to pay CIT bonds, is deposited directly from Cook County to a trustee. Because of this set-aside requirement, the majority of the appropriations for FY2021 will be paid from revenues set aside in FY2020. Table 1 provides information on the debt service fund balance at the beginning of the year, the expenditures that are made from the debt service fund, and the revenues that largely fund the debt service requirements for the following fiscal year.

| FY2019 Actual |

FY2020 Estimated |

FY2021 Budget |

|

|---|---|---|---|

|

Beginning Fund Balance |

785.5 |

774.0 |

758.0 |

| Revenues | |||

|

Property Taxes |

30.3 |

0.0 |

0.0 |

|

PPRT |

34.9 |

64.3 |

39.4 |

|

EBF |

282.7 |

381.9 |

445.6 |

|

Federal Interest Subsidy |

24.9 |

24.8 |

24.8 |

|

Other Local (City IGA and Net of Interest Earnings) |

140.2 |

152.35 |

152.3 |

|

CIT |

46.7 |

51.1 |

51.1 |

|

Total Revenue |

559.7 |

674.4 |

713.2 |

| Expenses | |||

|

Existing Bond Principal payment |

112.7 |

186.0 |

190.6 |

|

Existing Bond Interest payment |

514.2 |

499.6 |

519.5 |

|

Fees |

2.7 |

1.86 |

0.5 |

|

Total Existing Bond Debt Service |

629.6 |

687.4 |

710.5 |

| Other Financing Sources | |||

|

Net Amounts from Debt Issuances |

58.7 |

(2.5) |

0 |

|

Transfers in /(out) |

(0.3) |

(0.5) |

(0.5) |

|

Total other Financing Sources /(Uses) |

58.4 |

(3.0) |

(0.5) |

|

Ending Fund Balance |

774.0 |

758.0 |

760.1 |

Future Debt Service Profile

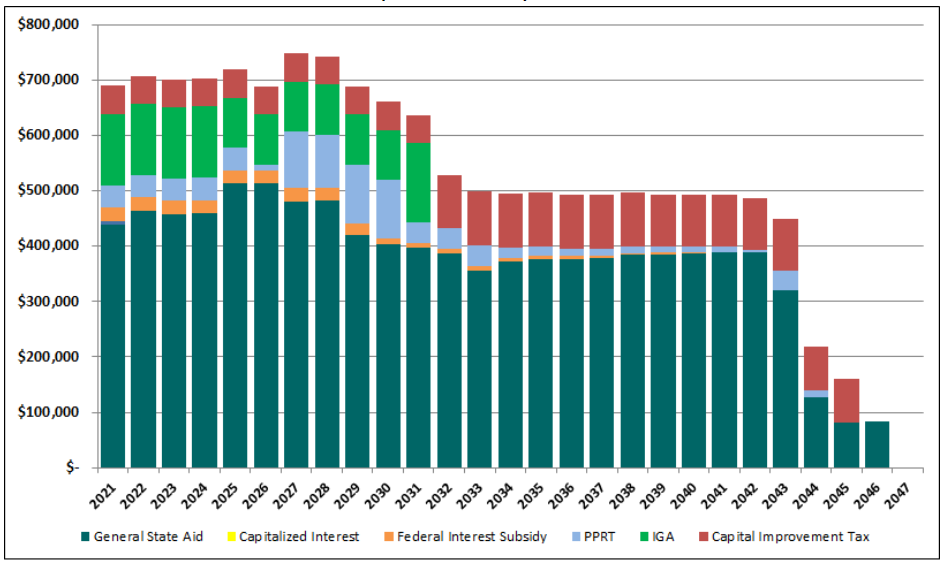

The following graph illustrates CPS’ debt obligations on outstanding bonds as of June 30, 2020. This graph does not show the impact of any future bonds required to support future capital budgets or debt restructuring.

Chart 1: CPS Debt Service Funding Schedule

(as of June 30, 2020)

($ in Thousands)

Note: Does not include future long-term bond financings or current and future short-term financings

Measuring Debt Burden

External stakeholders, such as taxpayers, employees, parents, government watchdog groups, rating agencies, and bondholders, frequently review CPS’ debt profile to gauge its size and structure as a crucial component of CPS’ financial position. In addition to evaluating the total amount of debt outstanding and the annual debt service payments, external stakeholders also look at the “debt burden” to gauge how much taxpayers bear in debt costs and determine how much debt is affordable for residents, which establishes true debt capacity. Several methods of measuring debt burden are commonly employed for school districts, including comparing existing debt to legal debt limits, measuring debt per capita, and measuring debt as a percentage of operating expenditures.

Legal Debt Limit

The Illinois School Code imposes a statutory limit of 13.8 percent on the ratio of the total outstanding property tax-supported debt a school district may borrow compared with a school district’s equalized assessed value, which generally represents a fraction of total property value in the district. Because the Board has issued alternate revenue bonds for which property tax levies are not extended, these bonds do not count against the legal debt limit imposed by the Illinois School Code. Therefore, total property tax supported debt is extremely low, at less than one percent of the legal debt limit.

Debt Per Capita

The Board’s per capita debt burden, or total debt divided by the City of Chicago’s population, has increased in the last decade. As reported in the FY2019 Comprehensive Annual Financial Report, General Obligation debt per capita is $2,691. This is still considered moderate to slightly above average relative to other comparable school districts. The Debt Management Policy is available at the Board’s website at policy.cps.edu.

| Description |

Closing |

Maturity |

Principal |

Pledged Funding |

|---|---|---|---|---|

| ULT GO Series 1998B-1* | 10/28/98 | 12/01/31 | 210,846,004 | IGA / PPRT |

| ULT GO Series 1999A* | 02/25/99 | 12/01/31 | 299,053,453 | IGA / PPRT |

| ULT GO Series 2005A | 06/27/05 | 12/01/32 | 143,665,000 | PPRT / EBF |

| QZAB Series 2006A | 06/07/06 | 06/01/21 | 6,852,800 | EBF |

| ULT GO Series 2006B | 09/27/06 | 12/01/36 | 22,005,000 | EBF |

| ULT GO Series 2009D | 07/29/09 | 12/01/22 | 9,650,000 | EBF |

| ULT GO BAB Series 2009E | 09/24/09 | 12/01/39 | 497,545,000 | EBF / Federal Subsidy |

| ULT GO QSCB Series 2009G | 12/17/09 | 12/15/25 | 254,240,000 | EBF |

| ULT GO QSCB Series 2010C | 11/02/10 | 11/01/29 | 257,125,000 | EBF / Federal Subsidy |

| ULT GO BAB Series 2010D | 11/02/10 | 12/01/40 | 125,000,000 | EBF / Federal Subsidy |

| ULT GO Series 2010F | 11/02/10 | 12/01/31 | 119,495,000 | EBF |

| ULT GO Series 2011A | 11/01/11 | 12/01/41 | 402,410,000 | EBF |

| ULT GO Series 2012A | 08/21/12 | 12/01/42 | 468,915,000 | EBF |

| ULT GO Series 2012B | 12/21/12 | 12/01/35 | 109,825,000 | EBF |

| ULT GO Series 2015CE | 04/29/15 | 12/01/39 | 280,000,000 | EBF |

| ULT GO Series 2015E | 04/29/15 | 12/01/32 | 20,000,000 | EBF |

| ULT GO Series 2016A | 02/08/16 | 12/01/44 | 725,000,000 | EBF |

| ULT GO Series 2016B | 07/29/16 | 12/01/46 | 150,000,000 | EBF |

| CIT Series 2016 | 01/04/17 | 04/01/46 | 729,580,000 | CIT |

| ULT GO Series 2017A | 06/13/17 | 12/01/46 | 285,000,000 | EBF |

| ULT GO Series 2017B | 06/13/17 | 12/01/42 | 215,000,000 | EBF |

| CIT Series 2017 | 11/30/17 | 04/01/46 | 64,900,000 | CIT |

| ULT GO Series 2017C | 11/30/17 | 12/01/34 | 328,875,000 | EBF |

| ULT GO Series 2017D | 11/30/17 | 12/01/31 | 74,035,000 | EBF |

| ULT GO Series 2017E | 11/30/17 | 12/01/21 | 22,180,000 | PPRT |

| ULT GO Series 2017F | 11/30/17 | 12/01/24 | 147,450,000 | IGA |

| ULT GO Series 2017G | 11/30/17 | 12/01/44 | 126,500,000 | PPRT / EBF |

| ULT GO Series 2017H | 11/30/17 | 12/01/46 | 280,000,000 | PPRT / EBF / IGA |

| ULT GO Series 2018A | 06/01/18 | 12/01/35 | 552,030,000 | EBF |

| ULT GO Series 2018B | 06/01/18 | 12/01/22 | 10,220,000 | EBF |

| ULT GO Series 2018C | 12/13/18 | 12/01/32 | 442,580,000 | EBF |

| ULT GO Series 2018D | 12/13/18 | 12/01/46 | 313,280,000 | PPRT / EBF |

| CIT Series 2018 | 12/13/18 | 12/01/46 | 86,000,000 | CIT |

| ULT GO Series 2019A | 09/12/19 | 12/01/30 | 225,283,872 | IGA |

| ULT GO Series 2019B | 09/12/19 | 12/01/33 | 123,795,000 | EBF |

| Total Principal Outstanding | $8,128,336,129 |

| Description | Maturity Date | Principal Outstanding | Pledged Funding Source for Debt Service |

|---|---|---|---|

| Tax Anticipation Notes, Series 2019B | 12/31/20* | 500,000,000 | Ed Fund Property Tax |

| Total Principal Outstanding | $500,000,000 |

Note: The maturity date of the 2019B TANs is the earlier of (A) December 31, 2020 or (B) the 60th day following the Tax Penalty Date.

| Fiscal Year ending June 30 | Total Existing General Obligation Bond Principal | Total Existing General Obligation Bond Interest | Total Existing G.O. Bond Debt Service | Total Existing G.O PBC Leases | TOTAL |

|---|---|---|---|---|---|

| 2021 | 222,381 | 430,703 | 653,084 | 653,084 | |

| 2022 | 252,078 | 425,051 | 677,129 | 677,129 | |

| 2023 | 258,017 | 413,722 | 671,739 | 671,739 | |

| 2024 | 297,182 | 412,111 | 709,293 | 709,293 | |

| 2025 | 323,024 | 402,984 | 726,008 | 726,008 | |

| 2026 | 313,246 | 383,463 | 696,709 | 696,709 | |

| 2027 | 317,653 | 439,372 | 757,025 | 757,025 | |

| 2028 | 285,949 | 404,260 | 690,209 | 690,209 | |

| 2029 | 298,038 | 402,468 | 700,506 | 700,506 | |

| 2030 | 237,076 | 386,695 | 623,771 | 623,771 | |

| 2031 | 263,066 | 337,290 | 600,356 | 600,356 | |

| 2032 | 195,050 | 221,461 | 416,511 | 416,511 | |

| 2033 | 205,115 | 210,912 | 416,027 | 416,027 | |

| 2034 | 195,005 | 202,310 | 397,315 | 397,315 | |

| 2035 | 211,140 | 189,139 | 400,279 | 400,279 | |

| 2036 | 223,290 | 171,429 | 394,719 | 394,719 | |

| 2037 | 232,370 | 164,694 | 397,064 | 397,064 | |

| 2038 | 246,265 | 152,069 | 398,334 | 398,334 | |

| 2039 | 260,930 | 137,705 | 398,635 | 398,635 | |

| 2040 | 276,830 | 122,632 | 399,462 | 399,462 | |

| 2041 | 293,675 | 105,794 | 399,469 | 399,469 | |

| 2042 | 314,039 | 79,793 | 393,832 | 393,832 | |

| 2043 | 280,628 | 75,763 | 356,391 | 356,391 | |

| 2044 | 285,752 | 49,579 | 335,331 | 335,331 | |

| 2045 | 302,876 | 35,295 | 338,171 | 338,171 | |

| 2046 | 301,880 | 17,941 | 319,821 | 319,821 | |

| TOTAL | $ 6,892,555 | $6,374,635 | $13,267,190 | $0 | $13,267,190 |

Note: Table is based on budgeted debt service requirements to be deposited within each fiscal year. Excludes issues completed after June 30, 2020 and any future anticipated transactions which were included in the FY2021 budget.

|

Fiscal Year ending June 30 |

Total Existing CIT Bond Principal |

Total Existing CIT Bond Interest |

TOTAL |

|---|---|---|---|

|

2021 |

51,084 |

51,084 |

|

|

2022 |

51,084 |

51,084 |

|

|

2023 |

51,084 |

51,084 |

|

|

2024 |

51,084 |

51,084 |

|

|

2025 |

51,084 |

51,084 |

|

|

2026 |

51,084 |

51,084 |

|

|

2027 |

51,084 |

51,084 |

|

|

2028 |

51,084 |

51,084 |

|

|

2029 |

51,084 |

51,084 |

|

|

2030 |

51,084 |

51,084 |

|

|

2031 |

51,084 |

51,084 |

|

|

2032 |

51,084 |

51,084 |

|

|

2033 |

42,615 |

54,201 |

96,816 |

|

2034 |

45,000 |

51,964 |

96,964 |

|

2035 |

47,535 |

49,602 |

97,137 |

|

2036 |

50,205 |

47,106 |

97,311 |

|

2037 |

53,170 |

44,322 |

97,492 |

|

2038 |

56,260 |

41,414 |

97,674 |

|

2039 |

59,540 |

38,339 |

97,879 |

|

2040 |

63,010 |

30,417 |

93,427 |

|

2041 |

66,685 |

26,731 |

93,416 |

|

2042 |

70,565 |

22,829 |

93,394 |

|

2043 |

74,680 |

18,700 |

93,830 |

|

2044 |

79,040 |

14,328 |

93,368 |

|

2045 |

83,645 |

9,702 |

93,347 |

|

2046 |

88,530 |

4,804 |

93,334 |

|

TOTAL |

$880,480 |

$1,067,467 |

$1,948,397 |

Note: Excludes issues completed after June 30, 2020 and any future anticipated transactions which were included in the FY2021 budget.